Home > blog > International Transactions > Cross-border payments challenges 2026: UK business insights

Cross-border payments challenges 2026: UK business insights

Last update:

UK businesses moving into global markets face a high-stakes moment in 2026. Online sales will make up nearly 40% of all UK retail sales by 2026. That growth opens opportunities across sourcing, exporting and cross-border trading, but it also means payments can either protect your margins or silently erode them.

For UK e-commerce retailers, manufacturers and wholesalers trading overseas, the question isn’t just about expansion. It’s about how fast and cost-effectively you move money, how much visibility you have and how well you manage compliance and foreign exchange risk.

This article explores the main cross-border payment challenges UK businesses face in 2026 and offers practical ways to manage cost, speed, visibility and risk. It aims to help exporters, online sellers and service providers improve efficiency, maintain control and keep international operations running smoothly.

Key takeaways:

- Cross-border payments drive UK business growth: As more companies expand into international markets, managing global payments effectively has become critical for protecting margins and maintaining competitiveness

- Cost, speed and transparency remain top challenges: Many UK firms still deal with high fees, slow transfers and unclear costs when moving money abroad, making it harder to plan cash flow and maintain healthy supplier relationships

- Currency risk and compliance add complexity: Fluctuating exchange rates and evolving post-Brexit regulations continue to affect how UK businesses trade across borders, increasing the need for proactive financial management

- Fintech and automation offer faster, more innovative solutions: New digital platforms simplify international transfers, improve visibility and integrate directly with accounting tools, reducing errors and administrative effort

- The World Account simplifies cross-border payments: With WorldFirst’s World Account, UK businesses can collect, hold and send multiple currencies in one place, gaining control, transparency and confidence in every international transaction

Open a World Account today and optimise the opportunities for global growth.

Why cross-border payments matter in 2026 for UK businesses

International payments are critical for UK companies in 2026. With domestic markets maturing, overseas commerce is a key growth avenue – especially in e-commerce.

In fact, cross-border online sales are growing faster than domestic e-commerce. Analysts project global retail e-commerce revenue will reach around US$8 trillion by 2026, with cross-border transactions expanding at nearly twice the pace of overall e-commerce throughout the decade.

For UK sellers, this represents a huge opportunity: Signifyd reports that UK e-commerce cross-border sales increased 4% year-on-year recently, even as domestic online growth stagnated.

The broader economic trends reinforce this importance. The Bank of England notes that, thanks to the globalisation of trade and the growth of digital marketplaces, the total value of cross-border payments worldwide is expected to skyrocket from about US$150 trillion in 2017 to over US$250 trillion by 2027.

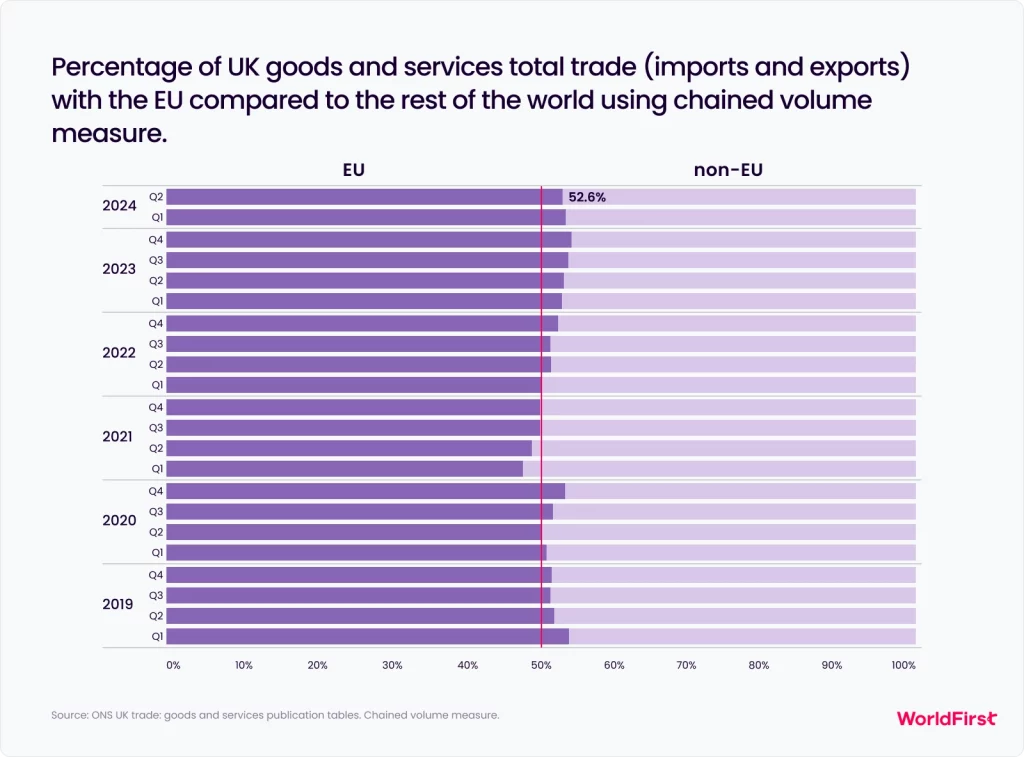

The EU remains the destination for roughly 41% of UK exports (goods and services) and trade with the US and fast-growing Asian markets continues to expand. From London boutiques selling across Europe to Midlands manufacturers sourcing from China, every business depends on smooth, cost-efficient cross-border payments.

Major cross-border payments challenges for UK firms

Cross-border payments remain slower, costlier and less transparent than domestic ones.

Here’s the key cross-border payment challenges in 2026 and why they matter:

1. High costs and FX pressure

Sending money abroad remains far more expensive than domestic transfers. Banks and intermediaries apply multiple layers of fees and FX markups, pushing total costs above 3% in many corridors. Smaller transfers, such as retail remittances, still average about 6% in fees.

The Bank of England notes that some cross-border payments cost up to 10 times as much as local payments. For SMEs, this directly eats into margins, particularly for e-commerce sellers converting overseas revenue during periods of sterling volatility.

2. Slow speed and settlement delays

International transfers often take days to clear through the correspondent banking network, especially when several currencies or intermediaries are involved. Weekends and differing bank holidays add further delays.

Even with improvements like SWIFT gpi tracking, only about 50% of cross-border payments globally reach the recipient within one hour and around 8% still take longer than a day to complete. These lags tie up working capital and disrupt supplier or customer relationships.

3. Lack of transparency

UK firms still struggle to see full costs and delivery times upfront. Each intermediary may deduct fees without notice and tracking a payment in transit can be difficult.

ACI Worldwide research shows that only 56% of payment services disclose complete cost and timing information. For finance teams, that uncertainty complicates reconciliation and cash-flow forecasting, especially when overseas refunds or supplier payments appear “stuck” for days.

4. Operational complexity

Managing cross-border transactions requires navigating multiple payment networks, country-specific formats and data requirements. Missing details, such as purpose codes, can trigger manual reviews or rejections.

Many businesses maintain separate foreign bank accounts to handle local currencies, which adds to administrative burdens and liquidity fragmentation. Global straight-through processing rates for B2B FX payments hover around 26%, indicating that much of the work still relies on manual steps.

5. Compliance and regulatory hurdles

Payments crossing borders undergo several layers of screening for AML, sanctions and fraud. Each bank in the chain runs its own review, often delaying legitimate transfers. Post-Brexit changes have added further complexity, with some EU institutions now classifying UK-EU euro payments as “international”.

Compliance requirements also drive up cost, as providers pass on expenses. Many firms must pre-fund accounts abroad to meet liquidity rules, locking up cash that could support operations.

6. Currency risk and volatility

Exchange rate swings can sharply impact profit margins. More than 54% of UK SMEs trading internationally reported losses from FX volatility last year, averaging £53,000 per business. Over half said a single poorly timed transfer cost them up to £20,000.

In response, around 58% of businesses have adjusted their FX strategies through hedging or invoicing in more stable currencies, yet exposure remains a key concern in 2026.

7. Cash-flow constraints

Finally, cross-border frictions tend to strain cash flow for businesses. When a payment is slow or held up for compliance checks, those funds aren’t available to use, which can hurt a small firm’s liquidity. Waiting five extra days for an overseas payment or pre-funding a foreign account with tens of thousands of dollars ties up working capital that the business could otherwise use.

For instance, a UK e-commerce merchant might have thousands in sales from a foreign marketplace that take weeks to settle and convert to GBP, making it difficult to pay suppliers or reinvest in inventory on time.

UK-specific context: policy, regulation and key corridors

Since Brexit, UK–EU transactions have faced higher costs and added complexity.

When the EU’s cap on interchange fees ended in 2021, Visa and Mastercard increased the rates on online card payments between the UK and the EEA from 0.2–0.3% to around 1.5% of the transaction value. As a result, UK e-commerce sellers now lose more to card fees on EU sales.

The UK–EU corridor remains the most significant for British firms, still representing roughly half of the UK’s foreign trade. While the UK stays part of SEPA, some banks now treat euro transfers as “international,” adding fees and delays. Businesses must also adjust to new VAT and data rules. Still, both UK and EU regulators are cooperating through the G20 roadmap to improve cross-border payment efficiency.

Beyond Europe, the United States remains the UK’s largest single trading partner, with exports of over £59 billion in 2024. Trade with China and East Asia is also rising as supply chains shift and new agreements, such as the CPTPP, open access to Asian markets.

Each corridor brings unique currency and regulatory factors. Ongoing work to connect the UK’s Faster Payments network with overseas instant-payment systems could soon make global transfers faster and more accessible for SMEs.

On the regulatory side, the FCA continues to strengthen AML and anti-fraud measures, improving safety but adding compliance steps. At the same time, projects like the Bank of England’s RTGS renewal and exploration of a digital pound (CBDC) could modernise how institutions settle international payments.

In short, UK businesses must keep pace with evolving policies and payment corridors. These changes influence the actual cost, speed and ease of sending money across borders.

Practical strategies for businesses to overcome cross-border payment challenges

Despite the challenges outlined, UK businesses aren’t powerless – there are concrete strategies and tools to make cross-border payments smoother and more cost-effective.

Here are some practical approaches:

1. Use multi-currency accounts to reduce FX costs

One of the simplest ways to avoid unnecessary conversion fees is to hold and pay in foreign currencies. A multi-currency business account – for example, the World Account from WorldFirst – lets you receive money in various currencies and store balances in those currencies.

This means a UK seller can collect euro or US dollar revenues into a local IBAN or US account, without each payment being auto-converted to GBP at poor rates. You can then wait for a favourable rate or batch conversions to get better deals.

Likewise, if you have suppliers in, say, China, paying them in CNH can skip intermediary conversions. By using a multi-currency account, businesses reduce the friction and frustration of dealing with multiple bank accounts and often eliminate inbound transfer fees. The result is more control over FX timing and significant savings on exchange margins.

2. Manage FX risk proactively

Currency swings can erode profit if left unmanaged. Lock in exchange rates with forward contracts, use hedging options or build FX buffers into your budgets. Many banks and fintech providers now offer SMEs the ability to fix rates for 6–24 months ahead, ideal for recurring supplier payments.

You can also request quotes in both GBP and the foreign currency to choose the better deal and avoid hidden markups. Dual-currency invoicing helps improve transparency and strengthens supplier trust. Over half of UK SMEs have already adjusted their FX strategies, proving that treating currency as a managed variable, not a gamble, makes a difference.

3. Use fintech and local payment networks

Traditional bank wires are no longer the fastest or cheapest route. Fintech payment platforms can process transfers through local banking networks, clearing funds domestically in the destination country.

UK fintech adoption rates are one of the highest in the world, higher than the global average of 64%. Using fintechs can shorten settlement times and cut costs, with many providers offering same-day or next-day delivery and upfront fee visibility.

Always compare spreads, since fintechs often provide tighter FX rates than high-street banks. Where possible, use tools such as SWIFT gpi tracking or open APIs to provide real-time updates. Choose the proper method for each corridor; in some cases, a marketplace or local fintech will move funds faster and more cost-effectively than a standard SWIFT transfer.

4. Integrate payments with accounting systems

Automation saves time and reduces errors. Link your cross-border payment tools directly to accounting platforms such as Xero or NetSuite to automatically reconcile multi-currency transactions.

This integration eliminates manual data entry, improves accuracy and provides real-time visibility across currencies. When evaluating financial software, ensure it supports multiple tax jurisdictions and currencies. Integration also helps consolidate international sales and payouts across marketplaces, giving finance teams one clear view of global cash flow.

5. Strengthen cash-flow management

Cross-border trade can easily strain liquidity, but proactive planning keeps operations running smoothly:

- Align payment timelines with international settlement cycles and negotiate realistic terms with customers and suppliers

- Add FX buffers in budgets to absorb currency swings between invoicing and payment

- Use trade finance or invoice financing to bridge gaps when waiting for overseas funds to clear

- Batch supplier payments into fewer, larger transfers to secure better FX rates and lower fees

Streamline approvals to remove internal delays and keep funds moving efficiently

Why WorldFirst leads among the best solutions for UK businesses

For UK companies tackling the specific challenges of 2026 – slow settlement, high cross-border costs, unclear fees and FX volatility – the World Account from WorldFirst turns payment complexity into a competitive advantage.

For UK importers, exporters and online sellers, the WorldAccount delivers what a modern global payments solution must: visibility, speed, cost control and international capability.

Instead of letting international payments erode margins silently, you can use the World Account to streamline supplier payments, convert when favourable and free up working capital for growth.

With the World Account, you can:

- Open local receiving accounts in 20+ currencies and collect payments like a local in key markets.

- Pay suppliers and partners in 100+ currencies, using faster local payment rails and avoiding SWIFT-chain delays

- Convert currencies when you choose, lock in rates ahead of time and gain complete FX visibility to protect margins

- Use deep integrations with major marketplaces (Amazon, Etsy, TikTok Shop) and accounting systems to achieve clean cash flow, simpler reconciliation and a single central dashboard

- Trade with confidence using a platform regulated by the UK’s Financial Conduct Authority and trusted by business users for international-scale payments

Overcome the cross-border payments challenges holding your business.

Open a World Account for free today and start managing global transactions faster, cheaper and with complete visibility across every market.

Sources:

- https://www.bankofengland.co.uk/speech/2023/cross-border-payments-opportunities-and-challenges

- https://www.fsb.org/2025/10/g20-roadmap-for-enhancing-cross-border-payments-2025-progress-report

- https://www.bis.org/about/bisih/topics/cross-border-payments.htm

- https://www.ons.gov.uk/businessindustryandtrade/internationaltrade/datasets/uktrade

- https://www.psr.org.uk/publications/review-of-interchange-fees-following-brexit

- https://www.ecb.europa.eu/press/key/date/2025/html/ecb.sp250401~9e1ee05e88.en.html

- https://www.mckinsey.com/industries/financial-services/our-insights/the-2025-global-payments-report

- https://www.innovatefinance.com/policy-blogs/the-key-to-unlocking-the-next-wave-of-growth-in-uk-fintech/

- https://remittanceprices.worldbank.org

- https://www.reuters.com/markets/currencies/visa-mastercard-interchange-fees-brexit-2023-09-27

- https://www.ft.com/content/7bfe3142-d98c-4aa5-964b-e85a92fa1cbe

- https://www.bloomberg.com/news/articles/2024-08-13/uk-smes-hit-by-sterling-volatility-report-warns

- https://www.swift.com/news-events/news/swift-gpi-tracker-transparency

- https://www.aciworldwide.com/cross-border-payments-landscape-challenges-and-innovations

- https://www.worldfirst.com/uk/

- https://www.worldfirst.com/uk/global-payments/world-account/

- https://www.worldfirst.com/uk/global-payments/netsuite-integration/

- https://www.currencycloud.com/company/news/industry-insight-cross-border-b2b/

- https://www.signifyd.com/blog/2025/05/03/uk-cross-border-ecommerce-growth-2025

Shawn Ma leads business development at WorldFirst UK, with a deep expertise in fintech, risk management and cross-border commerce.

Shawn Ma

Author

Continue reading

Subscribe

The Weekly Dispatch

Get the latest news and event invites. Signup for our weekly update from the worlds of fashion, design, and tech.

You might also like

Choose a product or service to find out more

E-commerce guides

Doing business with China

Exploring new markets

Business Tips

International transactions

E-commerce expansion guides

Doing business with China