Home > blog > Global Business Tips > Marketplace payments guide: How to manage payouts and fees [2026]

Marketplace payments guide: How to manage payouts and fees [2026]

Last update:

Marketplace growth has been intense, but the payment mechanics behind it often fall behind. For many businesses, the real challenge starts after the sale, when revenue moves from the marketplace to their own accounts. That gap is where fees, FX costs and cash flow uncertainty appear.

UK-based sellers often collect in GBP but pay suppliers in USD, EUR or CNY, which creates forced currency conversions and payout timing issues, making cash flow an everyday challenge.

Industry research consistently shows that well over half of e-commerce transactions now flow through marketplace platforms rather than standalone websites, with cross-border sales among the fastest-growing segments.

This guide focuses on how marketplace payments work in practice, explaining where fees and delays typically arise and how multi-currency payment flows help finance teams gain clearer visibility, access funds faster and stay in control as volumes scale.

Key takeaways:

- Marketplace payments break down after the sale, not at checkout: Delays, forced FX conversions and layered fees appear between sale and settlement, making it harder to turn revenue into usable cash

- Cross-border growth makes payout complexity unavoidable: Selling across multiple marketplaces and regions introduces different payout schedules, currencies and fee structures

- Fees add up quietly across the payment flow: While each fee may seem small, combined costs can take a meaningful share of revenue, especially for high-volume sellers

- Control comes from managing timing, currency and routing: Businesses that stay in control automate payouts, align payments with settlement cycles, reduce unnecessary transfers and treat FX decisions as part of margin management rather than a background process

- The World Account simplifies marketplace payments: With the World Account, businesses receive payouts locally, hold multiple currencies, pay suppliers directly and convert funds only when needed

Open a World Account for free and streamline marketplace payments as volumes grow.

The growing complexity of marketplace payments in 2026

Marketplace selling has changed faster than the payment systems supporting it.

As platforms such as Amazon, Etsy and AliExpress have expanded globally, businesses now collect revenue from multiple countries, in multiple currencies and on different payout schedules. What used to be a straightforward payment flow now involves multiple FX conversions, settlement delays and platform-specific fees.

According to Statista, global e-commerce sales are expected to exceed US$6 trillion by 2026, with cross-border trade accounting for a significant share of that total.

Many businesses still rely on traditional banking setups that do not fit this operating model. International transfers take days, FX pricing lacks transparency and fees stack up across platforms and banks, putting pressure on cash flow and margins.

Common challenges include:

- Currency exposure: Receiving and paying in multiple currencies introduces FX risk that can quietly impact profitability if not actively managed

- Delayed access to funds: Marketplace payout schedules and slow international transfers can leave revenue tied up when it is needed most

Layered fees: Conversion charges, cross-border fees and transfer costs accumulate across platforms and payment providers, reducing net returns

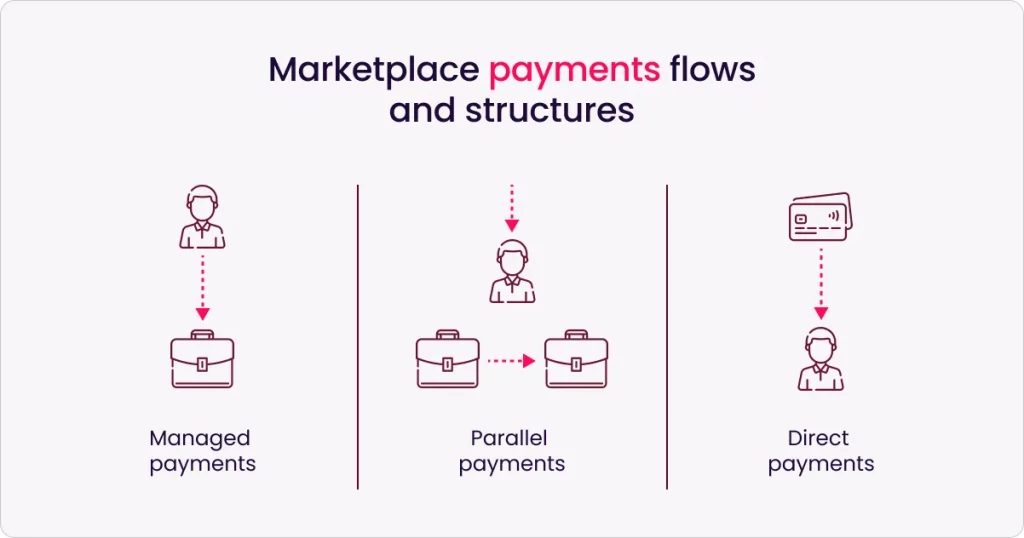

Managing payouts: streamlining marketplace operations

Marketplace payouts play a central role in day-to-day cash flow, yet they are often the least predictable part of selling online. Many businesses sell across multiple platforms simultaneously, each with different payout schedules, fees and reporting requirements. Sales may look strong, but turning that revenue into usable cash takes time and coordination.

Delays are the most obvious issue. Marketplaces release funds in batches rather than in real time and traditional banks can add further processing time and costs. This creates a gap between making a sale and being able to use the money.

Fees add another layer of complexity. Commissions, payment charges, FX costs and transfer fees appear across different reports, making it difficult to see the actual cost of each sale. As a result, cash flow planning becomes harder, even though supplier payments, inventory and operating costs still follow fixed schedules.

The impact of inconsistent payout structures

Each marketplace sets its own rules. Some release funds weekly, others biweekly or monthly and timing can vary by country or seller profile. Payment processors then apply their own pricing and settlement timelines on top of that.

For example, large marketplaces may hold funds for several weeks before releasing them, while payment providers charge a percentage-based processing fee and a fixed per-transaction fee. When businesses sell across multiple regions, those fees often include FX markups and cross-border transfer costs that apply after the payout leaves the marketplace.

Individually, these costs may seem manageable. Together, they add up to slower access to cash, higher operating costs and more manual reconciliation work. As sales volumes grow, these inefficiencies scale with them.

Practical ways to manage marketplace payouts more effectively

The right payment setup matters, but day-to-day payout management determines whether marketplace revenue supports growth or creates friction.

Businesses that stay in control use a set of practices that reduce uncertainty and keep cash available when it is needed:

1. Build automation into payout flows, not just reporting

Manual payout handling breaks down quickly as volumes grow.

Automating the flow of funds from marketplaces to your payment account and onward to suppliers or partners reduces the risk of missed payments and relieves pressure during peak trading periods. Automation also limits rework, since fewer manual steps mean fewer errors to correct later.

2. Plan supplier payments around settlement reality

Marketplace payout timing rarely aligns with supplier terms, which puts pressure on cash planning. Finance teams that understand each platform’s settlement cycle can schedule outgoing payments with confidence, rather than relying on short-term buffers or manual workarounds.

When payout timing is predictable, supplier relationships improve and cash planning becomes more stable.

3. Reduce unnecessary transfers with clear payout thresholds

Frequent small transfers create cost and noise without improving access to cash. Setting internal thresholds for when funds move helps consolidate balances, cut transaction fees and simplify reconciliation.

This approach works exceptionally well for businesses selling across multiple marketplaces with uneven sales volumes.

4. Treat FX as a margin decision, not a background task

Automatic currency conversion often happens at the worst possible moment, simply because a payout triggers it.

Holding funds in local currency and converting intentionally gives businesses control over timing and cost. Over time, this approach reduces unnecessary FX costs and makes margins easier to protect and forecast.

Understanding fees and how to reduce them

Marketplace payments come with layers of costs that businesses often overlook. When you sell internationally, fees apply at multiple stages, from the moment a customer pays to when funds reach your bank account or your suppliers.

Small percentages and fixed charges often look insignificant on their own, but at scale, they add up and make margins harder to manage. A 2–4% fee may seem manageable in isolation, yet combined fees can take a noticeable share of revenue, especially for high-volume sellers or businesses operating on tight margins.

The main types of fees in marketplace payments are:

1. Transaction fees

Payment processors and gateways typically take a cut every time a customer pays on your marketplace or checkout page. For example, standard card processing rates often fall around 2.9% plus a fixed per-transaction fee and costs rise for international cards or cross-border payments.

2. Currency conversion and FX fees

Whenever a payout arrives in a currency other than your base account currency, providers typically add a conversion fee to the mid-market rate.

These charges usually range from about 1–3% of the amount converted, though some services apply higher markups that quietly eat into your revenue if conversions happen by default after each payout.

3. Withdrawal and transfer fees

Moving funds out of a payment platform into a local bank (especially cross-border) can incur fixed transfer costs, intermediary bank or SWIFT fees and correspondent bank charges.

These can run from modest fixed amounts to tens of dollars per transfer on traditional banking rails.

4. Interchange and hidden network fees

Card networks apply interchange fees, which are charges banks pay when a card transaction occurs. These fees often make up the largest share of the costs merchants pay to accept card payments.

On top of that, acquiring banks and payment gateways may add their own charges, further increasing the total cost of each transaction.

Why these fees add up

When you sell across multiple marketplaces and in multiple currencies, costs compound quickly:

- You pay transaction fees on each sale

- Some marketplaces or gateways tack on cross-border or international processing surcharges

- Currency conversions happen automatically on receipt unless you can hold funds in the original currency

- Transferring funds across borders involves additional charges from banks or intermediaries

Practical ways to reduce the impact of fees

Fees are rarely the result of a single bad decision. They build up through routine payment choices that seem convenient at first but become costly as volumes grow.

Businesses that keep costs under control tend to focus on where fees enter the flow and make deliberate choices about timing, currency and routing:

1. Keep funds in their original currency for longer

Automatic currency conversion is convenient, but it is rarely optimal. When marketplace payouts convert as soon as they clear, businesses lose control over timing and rate. Holding funds in the original currency keeps options open.

Finance teams can convert when rates make sense, use those balances to pay overseas suppliers directly or move funds only when cash is actually needed. Over time, this approach reduces the cost of repeated conversions and yields more predictable margins.

2. Simplify the payment path

Every extra step between a marketplace and your final account adds cost and delay. Funds that move from a marketplace to a gateway, then through one or more banks, incur fees at each step.

Consolidating payouts into a single multi-currency platform shortens that path. Fewer handoffs mean fewer charges, faster settlement and less reconciliation work across systems that do not talk to each other.

3. Align transfers with real cash requirements

Moving money too often is rarely free. Frequent, low-value transfers may feel safer, but they usually trigger fixed fees each time funds move.

Planning transfers around actual business needs, such as payroll runs or supplier payment cycles, helps reduce unnecessary costs without tying up working capital. The goal is not to delay access to cash, but to move it with purpose.

4. Demand clarity on pricing

Fee structures should be easy to understand before costs appear on a statement. Some providers bundle charges into FX rates or apply cross-border fees with limited visibility, making it challenging to forecast net revenue.

Choosing payment partners that clearly display rates, charges and conversion costs enables finance teams to model costs accurately and avoid surprises as transaction volumes increase.

Key features of efficient marketplace payment solutions

Marketplace payment solutions need to support the realities of selling across platforms and borders. These are the features that matter most when managing payouts, fees and cash flow at scale:

1. Built-in multi-currency control

For businesses selling internationally, the ability to receive and hold multiple currencies is important. The real advantage lies in avoiding forced conversions and in choosing when to convert funds.

Holding balances in their original currency allows businesses to manage FX exposure, pay overseas suppliers directly and protect margins as volumes grow.

2. Faster access to marketplace funds

Delayed payouts slow down operations. Efficient payment solutions shorten the time between a sale and access to usable cash by reducing intermediary steps and, where possible, relying on local collection.

Faster settlement helps businesses restock inventory, meet supplier terms and respond to demand without relying on cash buffers.

3. Direct integration with marketplaces and platforms

Selling across multiple marketplaces quickly fragments payout schedules and reporting. Each platform follows its own settlement logic, making it harder to maintain a clear view of incoming revenue.

Payment solutions that integrate directly with e-commerce platforms help address this by:

- Bringing marketplace payouts into a single system

- Simplifying reconciliation across marketplaces and currencies

- Improving visibility into balances, fees and settlement timing

- Reducing the manual work involved in managing marketplace revenue

How the World Account supports marketplace payments in practice

Marketplace payments introduce complexity at three points: when businesses collect funds, convert them and pay them out again. The World Account from WorldFirst focuses directly on those pressure points.

At the collection stage, the World Account enables local receiving in major trading currencies, so marketplace payouts arrive without being routed through international wires. This shortens settlement times and avoids early FX conversions that occur when domestic accounts cannot hold foreign currency.

After funds arrive, businesses can hold balances in 20+ currencies in a single account. Finance teams can match inflows with outflows, pay overseas suppliers from existing balances or convert funds when timing and rates support cash flow goals, rather than converting automatically.

For outbound payments, the World Account lets businesses pay international suppliers directly from held balances. Fewer bank transfers reduce fees, shorten delays and simplify reconciliation across accounts and platforms.

In practical terms, the World Account helps marketplace sellers:

- Receive marketplace payouts locally in supported currencies rather than via international wires

- Hold and manage multiple currency balances in one account without automatic conversion

- Pay suppliers and partners overseas directly from those balances

- Convert currency only when needed, with visibility over rates and timing

- Reduce dependence on intermediary banks and fragmented payment setups

- Maintain a clearer view of available cash across marketplaces and regions

Finding it difficult to align marketplace payouts with supplier payments and cash needs?

Open a World Account for free and take control of marketplace payment flows across regions.

Sources:

- https://unctad.org/topic/ecommerce-and-digital-economy

- https://www.statista.com/topics/871/online-shopping/

- https://www.bankofengland.co.uk/markets/cross-border-payments

- https://www.bis.org/payments.htm

- https://www.ecb.europa.eu/paym/intro/html/index.en.html

- https://www.ukfinance.org.uk/policy-and-guidance/reports-and-publications

- https://www.fca.org.uk/firms/payment-services

- https://www.acfe.com/report-to-the-nations

- https://www.oecd.org/digital/

- https://www.worldbank.org/en/topic/paymentsystemsremittances

Abdul Muhit has 17 years' experience in banking and payments, spanning across regulation, payment networks, acquiring, issuing and treasury. He has served across strategic and delivery roles in product, technology and operations functions at global companies including JP Morgan, KPMG and Visa."

Abdul Muhit

Author

Continue reading

Subscribe

The Weekly Dispatch

Get the latest news and event invites. Signup for our weekly update from the worlds of fashion, design, and tech.

You might also like

Choose a product or service to find out more

E-commerce guides

Doing business with China

Exploring new markets

Business Tips

International transactions

E-commerce expansion guides

Doing business with China

The simpler way to pay and get paid

Save money, time, and have peace of mind when expanding your global business.