How to receive money with SGD account details in Singapore

Last updated: 9 Dec 2025

If your business trades in or with Singapore, getting paid in Singapore dollars (SGD) quickly and without complications is crucial. Marketplace sellers, exporters, SaaS providers, agencies and freelancers all aim for the same outcome: faster settlements, lower fees, clean reconciliation and no forced currency conversions.

Wondering how do I receive money with my SGD account details? This guide walks you through exactly how it works, locally and internationally. It presents what SGD account details are, how they work and how to use them to receive payments from local and overseas clients.

Also, it explains why many businesses now use the World Account by WorldFirst to simplify collections and reduce FX costs.

Key takeaways:

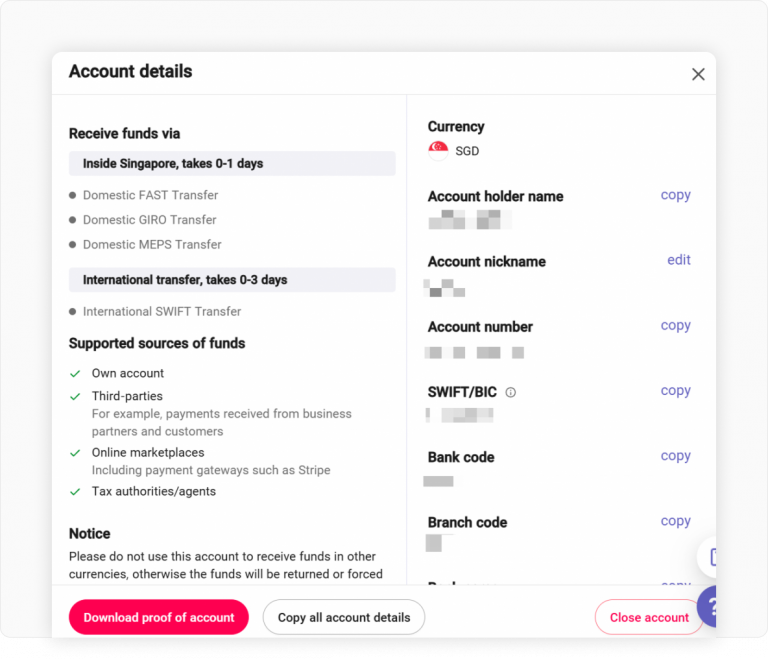

- Know your SGD account details: To receive money in Singapore dollars, you’ll need your account name, number, bank and branch codes and SWIFT/BIC code. Singapore doesn’t use IBANs, so accurate local details are crucial for smooth transfers

- Use FAST and PayNow for instant local payments: FAST offers 24/7 real-time transfers up to SG$200,000, while PayNow Corporate lets businesses receive payments instantly using a UEN or QR code

- Handle international transfers efficiently: Overseas clients can pay via SWIFT, but it often involves fees and delays. A better solution is to use a multi-currency account that gives you local payment details in different countries and lets you convert funds when exchange rates are favourable

- Simplify your global payments with the WorldFirst World Account: The World Account lets Singapore businesses receive, hold and convert over 20 currencies with no monthly fees or minimum balances

Open a World Account and start receiving payments in Singapore today.

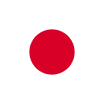

What are SGD account details?

SGD account details refer to the banking information you provide to someone who wants to pay you in Singapore dollars. In Singapore, bank accounts don’t use IBANs (International Bank Account Numbers) – instead, local transfers rely on a bank code, branch code and account number.

Typically, your SGD account details will include:

- Account name: The name of the account holder (your company or personal name)

- Bank name and branch: For example, DBS (Development Bank of Singapore) Marina Bay branch

- Bank code and branch code: A 4-digit bank code and 3-digit branch code identifying your bank and branch

- Account number: The unique number for your account (usually 7-11 digits in Singapore)

- SWIFT/BIC code: For international transfers, Singapore banks use an 8- or 11-character SWIFT code (also known as a BIC) instead of an IBAN. For instance, DBS Bank’s SWIFT code is DBSSSGSG. Singapore does not use IBANs or domestic routing numbers for its local banking system

You receive these details when you open a business account in Singapore. If you use a multi-currency fintech account, you may receive “virtual” local SGD account details (often in your business name or with a unique reference).

These details function like a regular local bank account, allowing you to receive SGD payments from Singaporean customers via domestic transfer networks.

Receiving money locally in SGD

When both the sender and recipient are in Singapore, the quickest way to receive SGD is via domestic instant payment networks.

Here is how local SGD receipt flows work:

1. FAST (Fast And Secure Transfers)

FAST is Singapore’s 24/7 real-time interbank transfer system. If someone transfers money to your SGD account via FAST, the funds typically arrive within seconds.

The sender will input your bank and account number in their internet or mobile banking app to send you money. FAST can handle both personal and business payments, with each transfer up to SG$200,000.

For the vast majority of business payments, SG$200k per transfer is more than sufficient. Suppose a client needs to pay you a substantial sum above that limit. In that case, they can either split it into multiple FAST transfers or use Singapore’s high-value payment system (MAS MEPS+ real-time gross settlement) for a single large transaction.

FAST is free or low-cost for businesses. Many banks offer several free FAST transfers for business accounts each month and it has essentially replaced the older, slower interbank GIRO for most needs.

2. PayNow and PayNow Corporate

PayNow is an overlay service on FAST that lets payers send SGD instantly using a proxy identifier instead of bank account numbers.

For individuals, that proxy can be a mobile number or NRIC. For businesses, PayNow Corporate allows linking your SGD account to your Unique Entity Number (UEN) and even generating an SGQR code for payments.

Customers can pay your business by entering your UEN or scanning a QR code, without you needing to share your account number. Funds still move via FAST, so they arrive instantly into your account.

More than half of Singapore’s population now uses PayNow regularly and as of 2025, 21 banks and more than five major e-wallets offer the service.

For businesses, this broad adoption is a big plus. You can collect payments from almost any customer seamlessly. PayNow Corporate was launched in 2018 and has since become universal. Therefore, nearly all Singaporean merchants (over 90%) can accept PayNow via SGQR codes.

Importantly, PayNow transfers in SGD are exceptionally cheap. Many banks charge no fee or a nominal SG$0.20 per transaction for businesses and even those small fees are often waived through 2025 to encourage cashless payments. In fact, DBS has confirmed that incoming PayNow payments to businesses will remain free until the end of 2025.

In short, using PayNow Corporate (UEN or QR) is one of the easiest ways to receive SGD locally. It’s instant, secure (bank-grade, MAS-regulated). Also, it simplifies reconciliation, as you can identify payments by the payer’s UEN/phone number or by attaching invoice references.

3. GIRO and direct debit

Before FAST, the Interbank GIRO system was the standard for business payments, such as payroll and vendor transfers.

GIRO is a batch-based system (not real-time) that takes 1–2 working days for funds to clear. You might still encounter GIRO for recurring collections (e.g., clients may set up GIRO to pay you on fixed schedules). GIRO transfers require your bank code, branch code and account number and are typically free or just a few cents per transaction.

While reliable, GIRO is slower than FAST/PayNow, so it’s less common for urgent payments. It remains useful for scheduled payments or legacy processes, but note that Singapore’s payment modernization means even recurring payments are moving to instant methods.

4. Cheques (being phased out)

Historically, businesses in Singapore often received payments by cheque (paper check).

However, Singapore is rapidly moving toward a cheque-free economy. The Monetary Authority of Singapore announced a timeline to eliminate corporate cheques by the end of 2026, pushing companies to adopt electronic transfers.

In practice, you should encourage clients to pay via FAST or PayNow instead of issuing a cheque. Not only are cheques slow (typically taking 2–3 days to clear and requiring manual deposit), but they’re also now costly since banks have introduced higher cheque processing fees to discourage their use.

- Open 20+ local currency accounts and get paid like a local

- Pay suppliers, partners and staff worldwide in 100+ currencies

- Collect payments for free from 130+ marketplaces and payment gateways, including Amazon, Etsy, PayPal and Shopify

- Save with competitive exchange rates on currency conversions and transfers

- Lock in exchange rates for up to 24 months for cash flow certainty

Receiving money internationally in SGD

What if your client or business partner is overseas but needs to pay you in SGD? This typically involves an international wire transfer into your Singapore bank account.

Here’s how to navigate international SGD receipts:

1. SWIFT transfers to your SGD account

The standard method for cross-border payments is the SWIFT network, also known as a telegraphic transfer (TT).

To receive an overseas payment into your SGD account, you must provide your SWIFT/BIC code (for example, UOB’s SWIFT code is UOVBSGSG), along with your account name, account number, bank name and branch address. The overseas sender’s bank will route the payment through correspondent banks to your Singapore bank.

Once the money arrives, your bank credits your SGD account. International SWIFT transfers usually take 1–3 business days to reach you (sometimes longer if multiple intermediary banks are involved). Keep in mind that banks along the way may deduct fees from the amount. It’s common to lose SG$20–$30 (or more) in intermediary charges on a SWIFT payment, unless the sender chooses an “OUR” (sender pays all fees) option.

Tip: To avoid unnecessary conversion costs, ask the payer to send SGD if they have SGD available. For example, a partner in Europe can instruct their bank to remit in SGD (letting their bank handle the FX), so you receive SGD without your Singapore bank converting EUR to SGD. However, often the sender’s bank might not offer a great FX rate.

2. International FAST connections

Singapore is also building linkages between its domestic real-time system and those of other countries.

Notably, in 2023, the PayNow-UPI linkage with India went live, allowing instant low-value transfers between Singapore and India using mobile numbers/VPAs. Similar links with Thailand’s PromptPay and Malaysia’s DuitNow are in progress or pilot.

However, these services are currently limited to person-to-person transfers and relatively low caps (e.g., SG$1,000/day for the India link at launch). They’re great for remittances, but for business payments above a few thousand dollars, SWIFT or multi-currency accounts remain the practical solution for now.

3. Intermediary timelines and tracking

If you do use SWIFT, note that each bank in the chain might hold the funds briefly.

Thanks to improvements like SWIFT gpi, many transfers can be tracked and arrive faster (over 50% of SWIFT gpi payments globally reach the beneficiary within 30 minutes, according to SWIFT).

Still, always ask your overseas sender to get an MT103 receipt or transfer reference.

4. Using multi-currency accounts for foreign payments

A practical alternative to a direct SWIFT transfer is to receive funds through a multi-currency account. These accounts allow businesses in Singapore to hold and receive payments in multiple currencies while providing local account details in key markets such as the United States, the eurozone, the United Kingdom, Australia and Hong Kong.

When an overseas client pays you, they can send a local transfer in their own currency, avoiding international wire fees and delays. The funds appear in your account balance in that same currency and you can decide when to convert them to SGD at a competitive exchange rate or keep them for future use.

This method eliminates most SWIFT fees, shortens settlement times and ensures you receive the full amount without deductions from intermediary banks. It also gives you greater control over timing and exchange costs, making it an efficient way to collect payments from international clients.

Practical checklist: Receiving SGD payments

Keep payments flowing without errors or delays by following these steps:

1. Check your payment details

Confirm that your account name, number and (if needed) bank or branch code are accurate. Include clear payment instructions on every invoice. For local clients, add your PayNow UEN or QR code for faster transfers.

2. Set preferred payment methods

Tell clients the easiest and cheapest ways to pay you. For Singapore-based payers, recommend FAST or PayNow. For overseas clients, provide local account details in their currency when available to avoid SWIFT fees.

3. Clarify who pays fees

Agree in advance who covers transfer costs. For SWIFT payments, request the “OUR” option so the sender bears all fees and you receive the full amount. Local transfers typically avoid this issue.

4. Use payment references

Ask clients to include invoice numbers or short references when sending funds. FAST and PayNow both display these notes, making reconciliation simple and accurate.

5. Enable alerts and monitor inflows

Turn on notifications for incoming funds. Quick updates help you confirm receipt, follow up on missed payments and maintain visibility into cash flow.

6. Stay compliant and active

Keep your account verified and in good standing. Respond promptly to any KYC requests or documentation checks to prevent payment delays.

Benefits of using a multi-currency account: WorldFirst World Account

A multi-currency account can transform how your business in Singapore receives and manages SGD and other currencies. The WorldFirst World Account gives businesses a tailored multi-currency solution.

Here is why many SMEs choose the World Account over relying solely on a traditional bank account:

1. Local receiving details in multiple currencies

The World Account gives you local bank account details in many jurisdictions, including Singapore dollars and other major currencies. Clients overseas can pay your local account in their currency and the funds land in your World Account as if you had a local bank account in that country.

2. Faster and fee-free receipts

You can collect payments in 20+ currencies using the World Account, typically via local clearing networks (not SWIFT). Incoming payments incur no receiving fee and you avoid many of the hidden costs of intermediaries in traditional transfers.

3. Favourable exchange rates and currency conversion control

With the World Account, you can hold balances in multiple currencies and choose when to convert them. Forward contracts and locked-in rates are available (up to 24 months) for cash flow certainty. The FX margins are competitive too – up to 0.6% on major currency pairs.

4. Simplified global cash management

Rather than managing multiple overseas bank accounts, the World Account gives you a single dashboard to view all your currency balances. It integrates with accounting tools such as NetSuite and supports payment flows across multiple currencies.

5. No minimum balance and low entry barriers

Opening a World Account has no setup fee, no ongoing account maintenance fee and no minimum balance requirement in many jurisdictions. This makes it especially suitable for SMEs and freelancers scaling up.

6. Additional business tools and features

The World Account supports integrations with online marketplaces, batch payments, outgoing payments in 100+ currencies and debit cards for spending from your account balances.

Want to simplify how you receive money with SGD account details in Singapore?

Open a World Account for free and make receiving money with SGD account details in Singapore faster and easier.

How to receive money with SGD account details in Singapore

Learn how to receive money using your SGD account details in Singapore. A simple guide covering transfers, timings, fees, and best practices.

Dec / 2025

How to get paid from a US marketplace to a Singapore bank account

Find out how to receive US marketplace payouts into your Singapore bank account. Compare fees, transfer times, and the best payment options.

Dec / 2025

How do cross-border payments work in Singapore?

Discover how cross-border payments work in Singapore, the fastest transfer methods, key regulations, and the best ways to streamline payments.

Dec / 2025Businesses trust WorldFirst

- Almost 1,000,000 businesses have sent USD$300B around the world with WorldFirst and its partner brands since 2004

- Your money is safeguarded with leading financial institutions