- The RBA held the cash rate at 3.00% yesterday in a move widely expected by the market. The main course, however, was dished out in the accompanying statement with the board reiterating its easing bias. “The inflation outlook, as assessed at present, would afford scope to ease policy further, should that be necessary to support demand.” The board voiced a continued a lack of confidence towards global conditions stating, “Downside risks appear to have abated, for the moment at least”.

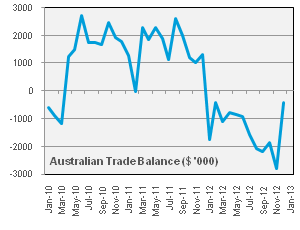

- Given the board’s more dovish stance, any significant weakness in Australian data may prompt a rate cut. Unlike January, the month ahead is void of quarterly data such as GDP and Inflation, potentially delaying a monetary response until within the second quarter.

- First and foremost, January employment data will be released on Thursday. Labour market conditions are expected to continue softening with 5,800 new jobs expected and the unemployment rate ticking up to 5.5%. Last month saw 5,500 jobs lost with a marked decrease in full-time employment; the most important component of the data. A leading indicator, ANZ Job Ads, was down 0.9% in January.

|