WorldFirst Home > blog > International Transactions > How to Receive International Payments: 3 Top Methods for Businesses

How to Receive International Payments: 3 Top Methods for Businesses

- Last update:

Receiving international payments—and managing money from overseas—can be a nightmare for many UK companies. Some problems that are far too common include:

- Payment delays. International payments using the SWIFT system can take up to three business days to clear in Europe—or even longer when coming from countries like China.

- High costs. Exchange rates vary each day, and banks and payment platforms charge a premium on top of the spot rate.

- Payment tracking and identification issues. Sometimes, money transfers get delayed due to fraud-detection systems, and others arrive without clear payer information, which can make accounting harder.

- Missing payments. In some cases, international payments can go missing completely. While most of these turn up eventually, they can cause serious anxiety in the meantime.

The alternative you have to managing international payments is to set up a local entity or banking relationship in each region where you operate. Yet this requires a lot of admin—particularly if you’re selling in many regions—as well as a deep knowledge of the local markets and their regulations.

So, is there a way to reduce the risk of these problems—or avoid them completely? In this guide, we share three key ways for businesses to receive international payments and better manage your finances.

We cover:

- How to receive international payments: 3 methods for businesses

- Multi-currency business accounts

- Cryptocurrency

- Conventional bank transfers

- How a World Account helps you save on international business payments

- How e-commerce startup Bull Doza collects payments internationally with WorldFirst

WorldFirst is a smarter, simpler way to manage global payments. With a World Account, you can start receiving international business payments in multiple currencies—and get paid like a local. Open an account for free today.

How to receive international payments: 3 methods for businesses

1. Multi-currency business accounts

One of the most reliable, affordable and fast ways to send and receive international business payments is with a multi-currency account.

As its name suggests, this is a type of payment platform that lets you use a single account to hold multiple currencies. You’ll get local account details in the currencies that you hold, so you can easily receive payments in the markets in which you’re selling.

This way, you’ll avoid the frustrations associated with conventional international payment methods. By holding local account details, you can bypass the SWIFT network, as your payments will be wired through local payment rails. The benefit is faster—and more affordable—payments.

The other benefit of these accounts is that they often come with competitive rates for foreign currency exchange and reduced transfer fees to bring your money back home. (However, be aware that every platform has its own rates—some better than others.)

With a World Account from WorldFirst, for example, you can open 20+ currency accounts, each with its own bank details, so you can accept payments in many currencies for free. You’ll also access low FX fees and receive your funds within the same day.

You can find out more about WorldFirst below. Or get started by opening a World Account today.

2. Cryptocurrency

An alternative—and increasingly popular—option to send and receive international business payments is cryptocurrency.

Cryptocurrencies such as Bitcoin and Ethereum are completely borderless currencies and so don’t require any foreign exchange conversions to be used in a different country. This means, if you use crypto to receive funds from overseas, you don’t need to think about exchange rates and you can avoid international transaction fees entirely.

That said, cryptocurrencies are notoriously volatile, as they’re not backed by any physical asset. Therefore, any payment you receive—or any funds that you hold—in crypto can radically shift in value, often overnight.

Plus, while crypto is increasingly adopted, you’ll likely find that this won’t be a viable solution for every single business payment. Simply, not everyone uses these currencies yet, and many people will likely want a more conventional alternative.

3. Conventional bank transfers

Bank transfers are the “original” way to make and receive international payments. For that reason, they remain the most common method for receiving funds from overseas.

However, it’s these conventional payments that suffer from most of the pain points we discussed in the introduction to this piece. Transfers to your current account typically use SWIFT, which can take up to six working days to process. Plus, banks charge an additional fee for these cross-border payments.

To receive funds via your bank, you’ll need to give the payer your International Bank Account Number (IBAN), and your Bank Identifier Code (BIC). Most overseas banks need both the IBAN and the BIC—which identifies your bank branch—to set up a transfer.

Alternatively, you can set up a local account in each country where you operate. However, to do this, you’ll typically need a local address in that country. This can be a major obstacle to many businesses.

How a World Account helps you save on international business payments

A World Account is a multi-currency account that empowers your business to grow beyond borders. You can get set up and start receiving international transfers—from 130+ marketplaces and payment processing gateways, as well as overseas buyers—in just a few minutes.

Unlike other multi-currency accounts, a World Account is completely free to set up and use to receive funds, with no ongoing account fees at all. When making international payments, a flat fee of £4 applies, which is waived for payments above £5,000.

Here are three reasons why you should use a World Account for your international business payments.

1. Get paid like a local in over 20 currencies

With a World Account, you can open over 20 local currency accounts, including in GBP, USD, CAD, AUD, CNH, EUR, HKD, JPY, NZD and SGD. You’ll be able to receive payments in these currencies for free—all in a single account.

What’s more, you’ll get local account details—including sort codes, account numbers, and IBANs—so you can get paid like a local in the markets in which you operate. This way, you don’t need an overseas address or established banking relationship in order to receive international funds.

This makes it much easier to:

- Set up operations in a new foreign market

- Collect earnings from marketplaces and payment gateways such as Amazon, Etsy, PayPal, and Shopify

- Receive funds from international buyers

- Get paid faster by leveraging domestic payment networks

Once you’ve been paid, simply transfer your funds into your home account or use your money to make domestic or international payments in the currency of your choice. For instance, you can make same-day or next-day payments to international or domestic suppliers, local tax authorities, or your employees—all in their preferred currency.

2. Access the best foreign exchange rates with our tools

When you want to send your money home, you’ll be able to take advantage of WorldFirst’s competitive currency exchange rates and pricing.

With a World Account, you can manage your currency conversion in the way that gets you the best rate. For instance, you can choose to exchange different currencies at today’s rate, one that you’ve chosen to lock in, or at a rate you want to wait for.

Plus, you don’t have to monitor exchange rates in real time yourself. Instead, you can set up alerts by email or text, so you’ll get notified whenever your target rate is reached. Alternatively, if you need to make a last-minute payment, you can do so easily with our live foreign exchange rates.

Receiving money shouldn’t come at a cost. With a World Account, you don’t have to give up part of your profits on currency payments and the fees commonly associated with cross-border transactions.

3. Start receiving funds in a matter of minutes

Registering for a World Account takes just minutes and can be done entirely online. Once your account is approved, you can set up receiving accounts in different currencies instantly. (You can find a step-by-step guide below.)

Then, to start getting paid, simply copy the details of your currency account and send them to customers—or connect your account to your e-commerce marketplace.

Plus, WorldFirst processes all payments on the day they’re made. If you’re sending money in GBP to your UK bank account—or EUR to your European bank account—your money typically arrives on the same day. It means no more waiting around for payments to clear—and better cash flow for your business.

If you already have an account that’s connected to a marketplace like Amazon or TikTok Shop, it couldn’t be easier to switch it to your World Account. As soon as you have an account with us, you can download an account verification letter to prove your ownership.

- Open 20+ local currency accounts and get paid like a local

- Pay suppliers, partners and staff worldwide in 100+ currencies

- Collect payments for free from 130+ marketplaces and payment gateways, including Amazon, Etsy, PayPal and Shopify

- Save with competitive exchange rates on currency conversions and transfers

- Lock in exchange rates for up to 24 months for cash flow certainty

How to set up a World Account and start receiving international payments

It’s really easy to get set up with a World Account. You don’t need to have a local presence to hold a particular currency, and it’s completely free to set up and start receiving international payments.

Here’s how you can get started so you can be paid like a local. Sign up here.

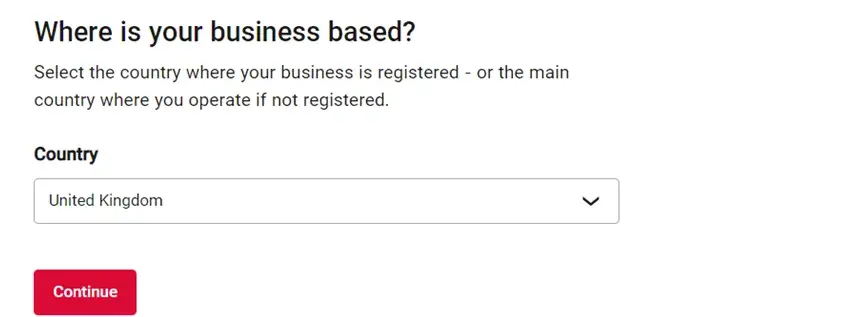

1. Gather all the information you’ll need and click ‘Sign Up’

Before you can set up your World Account, you’ll need some key information about your business and identity:

- Your ID (valid driving license or passport of the applying director)

- Valid ID copies for shareholders with 25% or more ownership

- Your company’s estimated monthly turnover

- Your company’s registration number, address, date and type

- The industry your company operates in

- Residential address of the applying director

- The full names and dates of birth of the current director(s)

- The residential address and shareholding percentage of the shareholders with 25% or more ownership

Once you have this information ready, simply click ‘Sign Up’ and select where your business is registered.

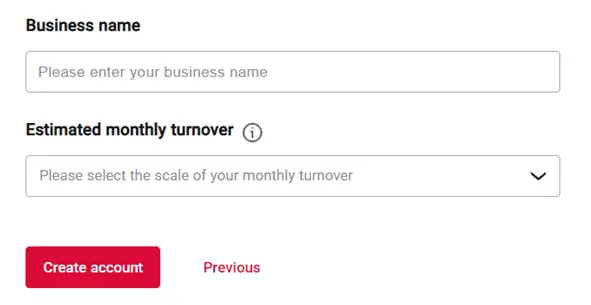

2. Create your account

Click ‘Continue’ and enter the email address you want to be associated with your account. You’ll receive a verification code and a link where you can set a password. You’ll need to then enter and verify your mobile number too.

After verification, select whether you’re a company or sole trader, before entering your business name and your estimated monthly turnover. At this point, you can click ‘Create account’. You should receive an email confirming that your account has been set up.

3. Verify your business details

To open any business account, you’ll need to verify your business details. To begin with, enter your company registration number, which can be found at Companies House.

Click ‘Next’ and confirm the basic information about your business (some of this will be pre-populated from Companies House). This includes your company name, type of business, registration date and trading address.

Then, confirm what you’ll be using your World Account for, select an industry, and enter your brand name. If you have a storefront or website, providing the URL can speed up your application.

It’s really important that all the information you provide in your application matches the information available on Companies House.

4. Complete some final identity checks

For anti-money laundering purposes, we need to verify your identity before we can finalise your account. For this, you’ll need your driving licence or passport. Simply scan the QR code and you’ll be able to take photos of your documents and face.

We’ll also need the names and dates of birth of all business directors and any shareholder who owns more than 25% of the business. You can upload copies of their documents in the next step.

At this point, all you need to do is click ‘Submit’. From here, it takes up to two days for us to review and approve your application.

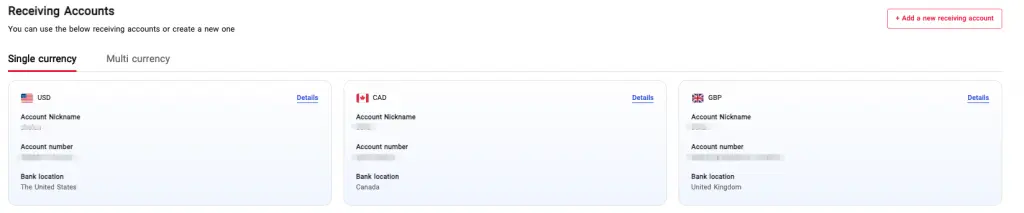

5. Set up a receiving account in any currency you want

To start receiving international payments, you’ll need to set up a currency account. This is a set of bank account details in your name that allows you to collect bank transfers. All balances will be reflected in your World Account.

As soon as you’ve set up a World Account, you can create a receiving account in over 20 currencies, including USD, EUR, GBP, AUD, CAD, HKD, JPY, SGD, NZD and CNH.

To create a receiving account, go to the Collection tab in your World Account dashboard. Then click on ‘Manage accounts’ and ‘Add a new receiving account’. You can then select the currency of your receiving account.

How e-commerce startup Bull Doza collects payments internationally with WorldFirst

Bull Doza Fight Wear is a UK-based manufacturer of high-quality martial arts equipment led by founder and director Nathaniel Doza. Bull Doza sells its products exclusively online, via e-commerce sites such as Amazon in the UK, US and EU.

However, the brand’s growth encountered some obstacles. To open a US Amazon account, Nathaniel needed local bank details for the US and EU—but the two different high street and neobanking providers he approached in the United Kingdom couldn’t offer them. In addition, uncertainties around foreign exchange costs made breaking into international markets daunting.

At this point, Nathaniel discovered WorldFirst. He was impressed by how easy it was to receive international payments:

- Bull Doza could print out a local account statement in seconds to use as proof when setting up a presence on local marketplaces in other countries

- On transfers of $10,000+, they saved an average of 1-3% compared to traditional banks

- They’re benefiting from exceptional transparency in exchange rates and transaction costs

Now, with WorldFirst’s help in entering new global markets, Bull Doza is confident about exploring opportunities overseas—and is aiming for a tenfold increase in sales.

Read the full case study: Bull Doza’s knockout move into global markets

Ready to receive international payments? Open a World Account for free today

If you’re breaking into a new market, or you have an international presence already, you’ll need a way to receive cross-border payments that’s affordable, fast, and fuss-free.

With a World Account from WorldFirst, you get exactly that. You’ll be able to:

- Open local currency accounts in 20+ currencies, all from a single, global account

- Accept international payments without the need for a local banking relationship

- Benefit from faster payments by using local payment networks

- Receive alerts when the target exchange rates are available, so you can maximise your profits when sending funds back home

Open a WorldFirst account today and start receiving international payments.

What is UK Export Finance and how can it help my business export overseas?

Discover what UKEF is and how it supports UK businesses with financing, insurance, and guarantees to help them win contracts and expand internationally.

Jun / 2026

9 best business cards for ad spend: compare top UK options

Discover the 9 best business cards for ad spend in the UK. See cashback rates, credit limits, fees, and perks to find the right card for your advertising budget.

Jun / 2026

6 top corporate virtual cards for global businesses

Virtual cards help you segment your spending when making payment online. In this guide, we share the top corporate virtual cards for businesses.

Jun / 2026WorldFirst articles cover strategies to mitigate risk, the latest FX insights, steps towards global expansion and key industry trends. Choose a category, product or service below to find out more.

- Almost 1,500,000 businesses have sent US$500B+ around the world with WorldFirst and its partner brands since 2004

- Your money is safeguarded with leading financial institutions