Home > Blogs > Business Tips

How to pick the best online business bank account (12 options)

Last update: 4 Jun 2025

Opening a business bank account should be simple. But for many businesses – particularly those selling across platforms like Amazon, eBay or TikTok – the reality is anything but.

Approval might take days or even weeks, and you might still be asked to visit a branch. Plus, if you want to open an account in another currency, you’ll often need to be a resident of that country for it to be possible.

Once you’re finally set up, you’re also likely to deal with:

- Limited online banking features or a user experience that isn’t very intuitive

- Fragmented visibility across currencies, accounts and other business finances

- Minimal customer support when things go wrong

- Delays on international transfers that slow down supplier payments

- Hidden FX markups that eat into already tight margins

- Manual reconciliation across marketplaces and regions

If any of these challenges sound familiar, this post is for you. We’ll walk you through:

- What to look for in an online business bank account (especially if you trade globally)

- Why WorldFirst is exactly what you’re looking for

- Comparison: WorldFirst vs other business bank accounts

- Other online business bank accounts to explore

Want to easily send money to suppliers around the world at low rates? Sign up to WorldFirst, the leading international bank account with transparent fees and fast setup.

What to look for in an online business account (especially if you trade globally)

While “online” accounts promise to make your life easier, many don’t actually do that. For instance, they still involve offline paperwork, outdated interfaces and long onboarding times.

If you’re looking for a UK business account you can open and run entirely online, here’s what to prioritise:

- Fast, fully digital setup – no paperwork, no branch visits. A truly online business account means you can apply, upload documents and get verified – all from your laptop or phone. Look for an account provider that promises end-to-end digital onboarding, with approval in one to two business days and no need to speak to a rep or visit a branch.

- 24/7 account access and management from anywhere. Whether you’re reviewing transactions or sending a last-minute payment, you should be able to manage everything from a central dashboard – no calls, no waiting. Features like mobile-friendly controls, real-time balance updates, and the ability to manage your account without needing to contact support are essential.

- Clear visibility and control over your finances. Digital accounts should make your money easier to track, not harder. That means they should provide a single login to see all your balances and seamless integrations within tools like Xero for accounting or reconciliation.

- No monthly fees or setup costs. You shouldn’t be charged just to keep your account open. A modern online account should be free to set up and maintain, with clear, transparent pricing for any extras like FX or transfers.

- Virtual cards you can issue instantly. Need to pay for Facebook ads, shipping, or SaaS tools? Virtual cards let you spend online in multiple currencies without waiting for plastic or paying extra FX fees. You should be able to issue them in seconds, assign each one to a specific platform, campaign or team member, and easily pause or cancel them if something changes. It’s a safer, more flexible way to manage business spending – and ideal if you want more visibility and control across multiple regions or tools.

- Responsive, human support. Just because the account is digital doesn’t mean support should be distant. Look for a provider with strong customer service, including real people on email or live chat when things go wrong.

- Bonus features that make running your online business easier. The best online accounts go beyond banking basics. Look for perks like:

-

- Local currency accounts you can open remotely, without local residency

- Fast international transfers without relying on SWIFT

- Direct integrations with Amazon, TikTok Shop, Shopify and other e-commerce platforms

These aren’t must-haves for every business – but if you sell online, advertise globally or pay international suppliers, they’re strong advantages.

Why WorldFirst is exactly what you’re looking for

If you’re after a business account that’s fast to open, easy to manage and built for online businesses – WorldFirst might just fit the bill.

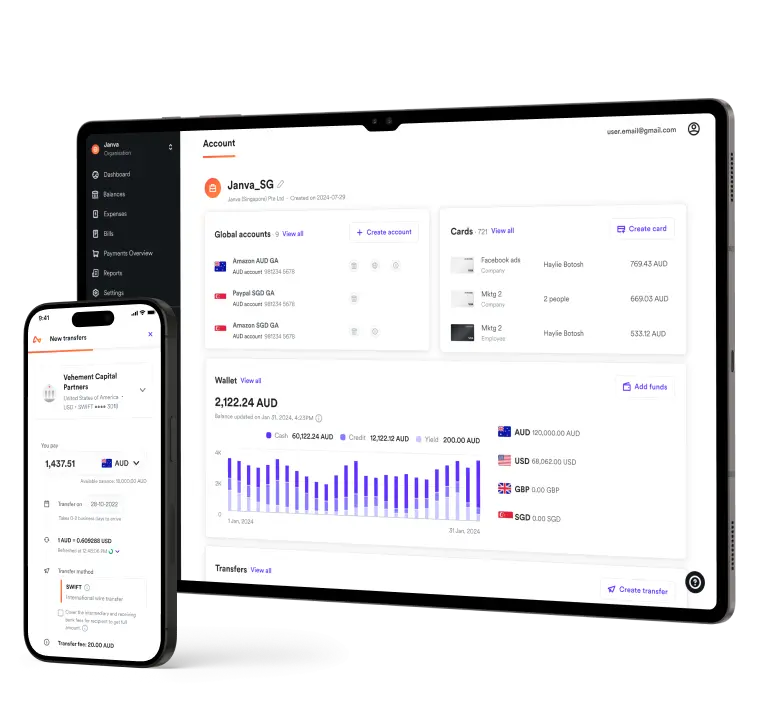

Our World Account is designed for businesses that sell and spend across borders – letting you manage multiple currencies, marketplaces, and payments from a single digital dashboard. Whether you’re collecting payouts from Amazon or paying suppliers in China, you get complete visibility and control in one place.

You can apply online and get approved in one or two business days with no paperwork and no branch visits. Then, start collecting e-commerce payouts from Amazon or TikTok Shop, hold funds in 20+ currencies, pay suppliers on 1688, and manage your global cash flow straight away online.

Here’s what you can do with the World Account:

Open 20+ local currency accounts without a local presence

With WorldFirst, you can open local receiving accounts in over 20 currencies – including USD, CNH, AUD, JPY, and AED – without needing to set up a local entity or be a resident in that country.

This is a game-changer for sellers on global marketplaces. Platforms like Amazon US, Shopee, or Rakuten often require a local currency account to receive payouts. Without one, you’re forced to route payments through intermediaries (often incurring transaction fees, delays, and poor FX rates) – or worse, you may not be able to sell at all.

WorldFirst solves this by giving you local-style bank account details (like a US ACH or EU IBAN), so you can collect funds directly, in local currency, from marketplaces and payment gateways.

No local paperwork. No expensive banking workarounds. Just full, free access to 20+ accounts from day one, via one central dashboard.

Why does local residency matter?

Most traditional banks – and even some fintech providers – require you to have local residency or a registered business entity in a country before you can open a bank account there.

That creates major friction for global sellers. For example:

- Want to receive USD payouts from Amazon US? You’ll often need a US bank account – which usually means a US address, tax ID, and local documentation.

- Selling to customers in Japan or the UAE? The same applies for JPY or AED accounts.

- Without local bank details, you may be blocked from listing products, face higher payout fees, or lose access to certain marketplaces altogether.

With a World Account, you can open 20+ local currency accounts from anywhere – no local entity, no in-person paperwork, no residency requirements. You get local bank details, just like a local business would use, making it easier to receive marketplace payouts, reinvest locally or transfer funds globally, and avoid intermediary fees or poor FX conversion rates.

It’s a faster, more flexible way to grow across borders.

Send international payments fast and at competitive rates

With WorldFirst, you can pay suppliers in over 100 currencies using local payment rails – including direct CNH payments to China. That means no SWIFT delays, no intermediary banks, and no inflated FX fees.

Here’s how it works:

When you send a payment through WorldFirst, the platform uses local banking infrastructure wherever possible. So instead of routing payments through a chain of correspondent banks (as with traditional SWIFT transfers), your funds are delivered directly and quickly – often on the same day or next day, depending on the destination.

If you’re paying Chinese suppliers, for example, you can:

- Send CNH payments directly to a supplier’s account

- Provide real-time proof of payment to suppliers – speeding up fulfilment

- Build trust with partners by paying in their preferred currency, quickly and transparently

You can also lock in FX rates ahead of time or set rate alerts to avoid margin loss when currency markets fluctuate – giving you more control over cash flow and cost planning. Unlike many providers, WorldFirst shows you the rate upfront and doesn’t add hidden markups into the exchange – so you know exactly what you’re paying.

Connect with 130+ marketplaces and payment platforms

With local account details, you can link directly with over 130 global marketplaces and payment platforms, including Amazon, Etsy, TikTok Shop, Shopify, PayPal, Stripe and more.

These integrations let you collect sales revenue in the local currency of each platform, without delays or detours through third-party services. You simply enter your World Account details into your seller portals and the payout lands automatically.

It’s a faster, cleaner setup for international sellers who use multiple channels. You don’t need to juggle accounts or chase payments across platforms – everything flows into one place, ready to convert, spend or withdraw when you need it.

Issue virtual cards and manage team spend

With WorldFirst, you can generate virtual cards instantly – perfect for online purchases like digital ads, SaaS subscriptions, or supplier payments.

Each card can be assigned to a specific team member, region, or campaign, making it easier to track where your money’s going. You can see spend in real time, manage limits per card and pause or cancel them with a click.

No more shared company cards or messy expense reports. Just smarter control over card payments – without waiting for plastic or paying extra FX fees.

Find out more: How a multi-currency virtual card helps your business grow

Comparison: WorldFirst vs. other business bank accounts

Here’s how WorldFirst stacks up on the features that matter most – from FX fees to onboarding ease.

| Provider | Currencies | Marketplace integrations | Local account opening | Transfer fees | TrustPilot |

|---|---|---|---|---|---|

| WorldFirst | 20+ | 130+ | No residency needed | From £0.30 | 4.0 (2,900+) |

| Wise Business | 9 receive / 50+ spend | Amazon, Etsy, Shopify | Limited (lets you receive funds – but may be restricted) | Setup fee + per transfer | 4.3 (250k+) |

| Revolut Business | 30+ | Shopify | UK-based only | FX markup tiers | 4.5 (200k+) |

| HSBC | 4 | None | UK only | SWIFT + monthly fees | 3.8 (12k+) |

| Monzo Business | 40+ | None | UK only | Free plan + Team £25 | 4.5 (47k+) |

| Payoneer | 10+ | Amazon, Upwork, Fiverr | Yes | Less transparent FX fees | 3.8 (58k+) |

| Starling Bank | 40+ | None | No | Mid-market + flat fee | 4.3 (44k+) |

| Barclays | 16+ | None | UK only | SWIFT + fees | 1.9 (12k+) |

| Juni | 5+ | Amazon, Shopify, Meta Ads, Google Ads | No | Up to 1.8% FX fee | 4.0 (400+) |

| Airwallex | 20+ | Shopify, WooCommerce | Yes | Low FX rates | 3.3 (1.7+) |

| Zempler | GBP, EUR | None | UK only | Domestic only | 3.8 (12K+) |

| N26 Business | EUR only | None | EU only | EU SEPA only | 3.3 (34k+) |

| Shopify Balance | GBP only | Shopify only | Shopify sellers only | Shopify only | 1.3 (3k+) |

| Tide Balance | GBP only | None | UK only | SWIFT + fees | 3.9 (24.5k+) |

TrustPilot ratings based on available data.

Other online business bank accounts to explore

If you’re still shopping around, here’s a longer list for business bank accounts and fintechs to compare.

1. Wise Business

Wise Business is a strong choice for freelancers and small businesses who regularly send or receive payments across borders.

It offers local receiving accounts in more than nine currencies – including USD, EUR, GBP, and AUD – and lets you send funds in over 40 currencies using real-time mid-market exchange rates. You can also connect Wise with e-commerce platforms like Amazon, Etsy, and Shopify, making it a convenient option for marketplace sellers.

However, Wise is not a licensed bank (so funds are protected by the Financial Conduct Authority (FCA) but not the FSCS) and some users report limited customer service for more complex queries or payment issues.

Learn more: https://wise.com/gb/business/

2. Revolut Business

Revolut Business is a digital-first account aimed at startups and SMEs looking for flexibility, speed, and a great user experience.

It supports payments in 30+ currencies and includes features like virtual cards, team spend controls, and built-in budgeting tools. You can integrate with Shopify and popular accounting platforms like Xero, making it a decent choice for digital-first teams.

However, FX fees apply unless you’re on a higher tier paid plan, and users often report delays in onboarding, re-verification requests, or account freezes. As of June 2024, Revolut is a licensed bank in the UK under a “restricted banking license”, meaning they’re still in a period of authorised activity with some limitations.

Learn more: https://www.revolut.com/business/

- Open 20+ local currency accounts and get paid like a local

- Pay suppliers, partners and staff worldwide in 100+ currencies

- Collect payments for free from 130+ marketplaces and payment gateways, including Amazon, Etsy, PayPal and Shopify

- Save with competitive exchange rates on currency conversions and transfers

- Lock in exchange rates for up to 24 months for cash flow certainty

3. Payoneer

Payoneer is a popular choice for freelancers, e-commerce sellers, and service providers receiving international payments, especially from platforms like Amazon, Upwork, and Fiverr. It offers local receiving accounts in multiple currencies (USD, EUR, GBP, JPY, and more), making it easier to get paid like a local across global marketplaces.

However, FX fees may be less transparent than other competitors, and users often face long account verification processes, limited customer support, or unexpected account holds. Like Wise, Payoneer isn’t covered under the UK’s Financial Services Compensation Scheme (FSCS).

Learn more: https://www.payoneer.com/business/

4. HSBC Business Account

HSBC Business Account is a traditional high-street option with global brand recognition and in-branch support. It offers multi-currency accounts (e.g. USD, EUR, CAD, HKD) and 12 months’ free banking for new customers.

However, it’s not built with modern e-commerce or international sellers in mind. You’ll need a UK presence to apply, marketplace integrations aren’t available, and international transfers typically run through SWIFT – meaning slower payments and higher fees. Onboarding can be slow, and FX margins are less competitive than fintech alternatives.

Learn more: https://www.business.hsbc.uk/en-gb/products/small-business-bank-account

5. Starling Bank

Starling Bank offers a modern, mobile-first business banking experience with no monthly account fees, FSCS protection (up to £85,000) and support for 40+ currencies via its international payments feature. It’s well-loved for its intuitive app, strong customer service, and real-time spending insights.

However, Starling is UK-focused and doesn’t offer local receiving accounts abroad – meaning you can’t get paid like a local in USD or EUR. There are also no marketplace integrations (e.g. Amazon, Etsy), and payments to China still go via SWIFT, which can slow things down and rack up costs for global sellers.

Learn more: https://www.starlingbank.com/business-account/

6. Monzo Business

Monzo Business offers a sleek, user-friendly interface with features like integrated invoicing, Xero and FreeAgent integrations, and 24/7 customer support. It’s a solid option for UK-based sole traders and small businesses looking for simple day-to-day banking with no monthly fees (on the Lite plan).

However, Monzo lacks multi-currency accounts and doesn’t offer local receiving accounts outside the UK. That means it’s not ideal for businesses selling internationally or needing to collect and hold funds in USD, EUR, or CNH. There are also no direct integrations with major marketplaces like Amazon or Etsy, and international payments rely on partner providers.

Learn more: https://monzo.com/business-banking/features

7. Barclays International Account

Barclays International Account is a well-established option for businesses seeking the credibility and breadth of a traditional high street bank. It offers foreign currency accounts in 40+ currencies and the backing of a global banking infrastructure.

However, opening an account typically requires a UK entity and may involve in-person verification and paperwork. There are no direct integrations with e-commerce platforms like Amazon or Shopify, and international transfers are routed via SWIFT, which can be slow and expensive. Monthly account fees and transaction charges apply after an initial free period. Best suited for larger businesses that value traditional banking relationships over digital-first features.

Learn more: https://international.barclays.com/

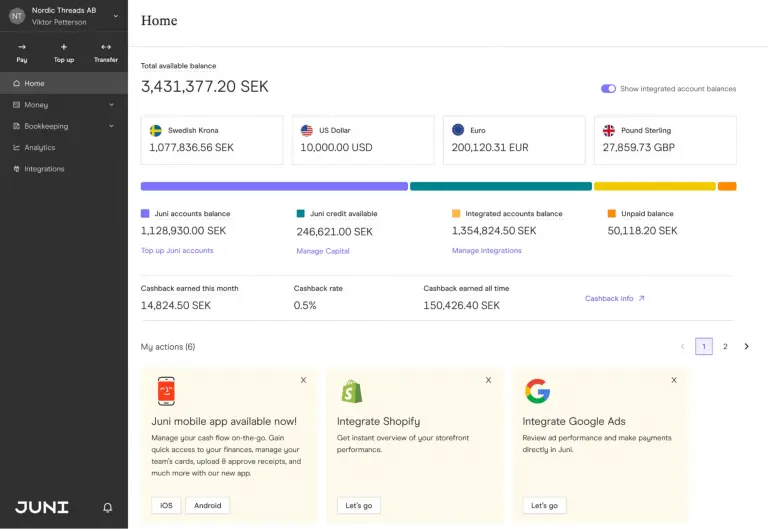

8. Juni

Juni is a financial platform tailored for digital marketers and e-commerce brands, offering integrated banking, cards, and financial management tools. You can hold and transact in 5+ currencies (GBP, EUR, USD, SEK, NOK), and integrate with platforms like Amazon, Shopify, Meta Ads, and Google Ads. The platform also offers virtual cards, expense tracking, and visibility over your ad spend.

However, Juni is not a traditional bank – it partners with regulated institutions for account services – and its basic plan starts at £19/month. International transfers can incur FX fees of up to 1.8%. Best for high-growth e-commerce businesses that want full visibility into marketing ROI, but less suited for those prioritising low-cost banking or wider marketplace integrations.

Learn more: https://www.juni.co/

9. Airwallex

Airwallex is a global payments platform built for modern businesses operating across borders. It offers multi-currency wallets in 60+ currencies, virtual and physical cards, and local account details in key markets including the US, UK, EU, Australia, and Hong Kong.

It supports batch payments, low FX rates, and integrations with platforms like Xero, Shopify, and WooCommerce. Airwallex is particularly strong for businesses operating in Asia-Pacific or working with Chinese suppliers.

However, it’s also not a bank (accounts are held through partner financial institutions) and some users have reported friction around compliance and onboarding. Best for startups and tech-savvy businesses with international operations that want enterprise-level payments infrastructure.

Learn more: https://www.airwallex.com/uk/business-account

Zempler

Zempler (formerly known as Crezco) is a UK-based business banking solution designed for SMEs. It offers a business current account with integrated invoicing, bill payments, and a built-in open banking layer that lets users connect directly to their accounting tools. Zempler focuses on helping businesses simplify payments and cash flow management, offering features like instant payment notifications, batch payments, and bank-grade security.

However, Zempler currently operates only in GBP and EUR and is not designed for complex international payment needs; there’s no multi-currency support or global receiving accounts. It’s best suited for UK-based businesses that need a simple, integrated, and regulated business account focused on domestic efficiency and accounting automation.

Learn more: https://www.zemplerbank.com/

11. N26 Business

N26 Business (EU only) is a digital-only bank based in Germany, available to freelancers and self-employed individuals across the EU and EEA. It’s a lightweight, mobile-first option that offers a free euro-denominated business account with included Mastercard, real-time notifications, and clean UX for managing everyday expenses.

It’s best suited to solo entrepreneurs who operate primarily within the eurozone, but may not be a fit for limited companies, teams, or businesses with global ambitions. There’s no support for receiving in other currencies, no bulk payments, and limited integrations with marketplaces or accounting tools. You also won’t get local account details outside the EU, making it a poor choice for international sellers.

Learn more: https://n26.com/en-eu/business-bank-account

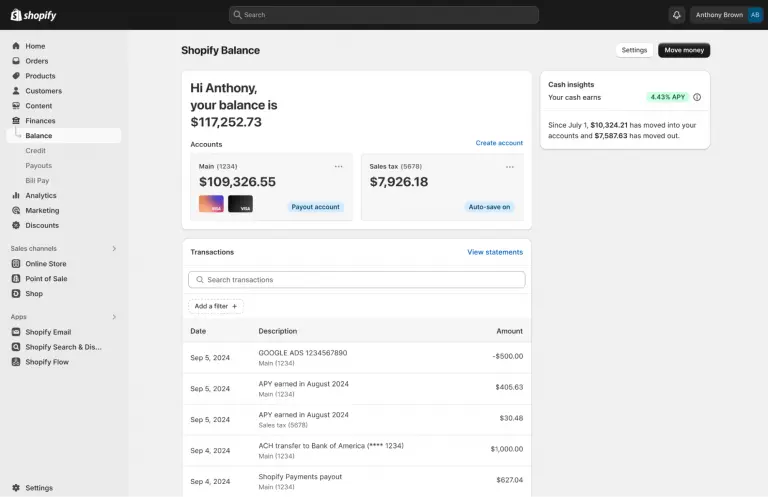

12. Shopify Balance

Shopify Balance is a financial product designed for merchants already selling through Shopify. It offers a built-in business account and debit card with fast access to sales revenue, especially useful for managing daily cash flow.

You can receive payouts from your Shopify store directly into your Balance account – often within one business day – and use the card for marketing, tools, or supplier purchases. It includes cashback rewards and no monthly fees for eligible users.

However, Shopify Balance is not a standalone business bank account. It’s only available to Shopify sellers, doesn’t support multi-currency accounts, has no SWIFT or international payment capabilities, and lacks connections to external marketplaces like Amazon or Etsy. If you’re selling across borders or on multiple platforms, you’ll need to pair it with a more global account like WorldFirst.

Learn more: https://www.shopify.com/balance

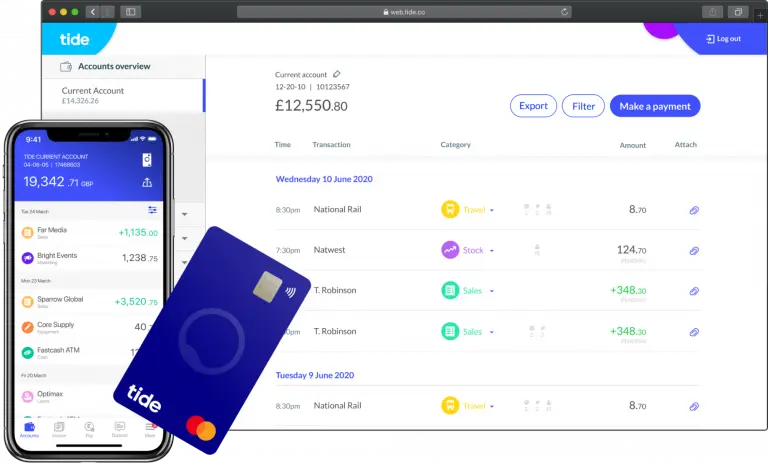

13. Tide Business

Tide Business is a UK-based digital banking platform tailored for sole traders and small businesses. It offers fast account setup, expense management tools, and seamless integrations with accounting software like Xero, FreeAgent, and QuickBooks.

Tide is particularly strong on user experience: you can open an account in minutes, issue team expense cards, and manage invoices directly from the app. There’s a free plan available, with paid tiers unlocking additional features like 24/7 support, automated expense categorisation, and cashback.

However, Tide doesn’t support multi-currency accounts or international payments beyond SEPA and SWIFT — which can be slow and come with extra fees. There’s also no support for global e-commerce sellers: no marketplace integrations, no local receiving accounts, and limited options for paying suppliers abroad.

If you’re looking to scale internationally or manage funds across borders, you’ll likely outgrow Tide’s domestic focus and need a more global-first solution like WorldFirst.

Learn more: https://www.tide.co/

Ready to open a WorldFirst account?

Join 1,000,000+ businesses who have sent $300B+ globally with WorldFirst. Open a free online business account in under 30 minutes and start managing international payments, collections, and currencies – all in one place.

WorldFirst articles cover strategies to mitigate risk, the latest FX insights, steps towards global expansion and key industry trends. Choose a category, product or service below to find out more.

- Almost 1,500,000 businesses have sent US$500B+ around the world with WorldFirst and its partner brands since 2004

- Your money is safeguarded with leading financial institutions