We have now updated our thoughts on INR for the 2nd half of the year. These are below:

Whilst large negative swings in emerging market currencies were widely predicted following the election of Donald Trump, in most cases they failed to materialise. The Indian rupee, however, was always thought to be one of the most resilient emerging market currencies and so it has proved. India has remained relatively insulated as, for all its size, it remains a relatively closed economy given capital controls on the currency and governmental oversight of inward investment. It also enjoys a relatively high savings ratio and low level of external financing.

We expect support for the INR to continue with the low level of volatility in global markets making carry trades whereby investors borrow and sell currencies at low interest rates and buy higher yielding currencies such as the INR, more popular.

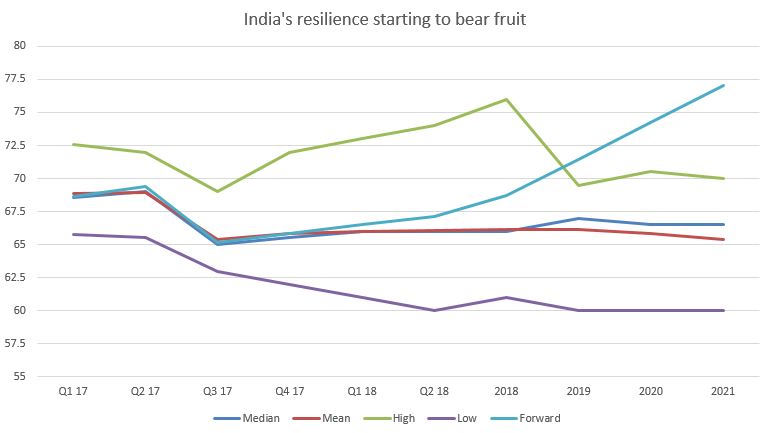

These predictions outline the high, low, median and mean expectations for the above currency pair as found by a Bloomberg survey of banks and brokers and should only be used for illustrative purposes. Source: Bloomberg

As you can see from the chart above the market expectation for USDINR is for it to remain around 66.00. At the beginning of the year we forecast that USDINR would trade between 64.00 and 68.00 and whilst that’s proved entirely correct so far, there is the chance that USDINR spends some time below 64.00.

If you were to rob a bank and ask for 86% of the bank notes in the building, you’d emerge with a lot of individual bills. India’s decision to monetise 86% of its bank notes, taking them out of circulation has caused an uproar in the country and will very definitely give pause to one of the most encouraging growth profiles in the emerging market space.

The plan was set in motion in the first place to eliminate the levels of blck money and cashless transactions in the economy and in the short term will paralyse spending and investment for members of the working class and agricultural and construction communities. In the longer term, as these transactions become more measurable and centralised then they should begin to meaningfully contribute to growth.

The natural side effect of this plan is to allow for the Indian government to more effectively call for and take in tax receipts from the newly banked workers. While this may not immediately translate into higher government spending, it will naturally improve the government’s fiscal position. A national Goods and Services Tax is due to be implemented from April 2017 and this may further contract economic activity as it is implemented.

The Reserve Bank of India has spent a lot of 2016 monitoring inflation and 2017 will be the same. The Bank’s range of contentment for price rises sits between 4-6% and current levels of price rises have sunk towards the lower end of this bound. As with a large majority of emerging markets, inflation is more closely tied to commodity markets than in developed markets courtesy of a higher proportion of wages being spent on fuel and food.

If global commodities stage a rally in 2017 amid a positive atmosphere for emerging market growth and developed market consumption, then a run towards the high side of the inflation range could easily materialise but market expectations of 25-50bps of interest rate cuts in 2017 seem about right.

But we cannot talk about emerging markets without mentioning Donald Trump however, whilst some markets are likely to feel a very chill wind from Washington once he steps into the Oval Office, we think that India will remain relatively insulated. India, for all its size, remains a relatively closed economy given capital controls on the currency and governmental oversight of inward investment while also enjoying a high savings ratio and low level of external financing. Also, the US has bigger fish to fry and weaker kids in the playground to pick on.

Hence we do not believe that INR will be definitively damaged by the strength of the US dollar and should remain in a USDINR range of 64.00-68.00 in the upcoming year.

Want to learn more? Check out our full list of 2017 currency predictions or drop us a line to research@worldfirst.com with any questions.