Brief Summary:

- The U.S. Fed continued tapering and delivered a dovish statement causing the USD to weaken and market calm to continue.

- The GBP strengthened as the Bank of England shifted rhetoric away from dovishness and toward the possibility of rate rises.

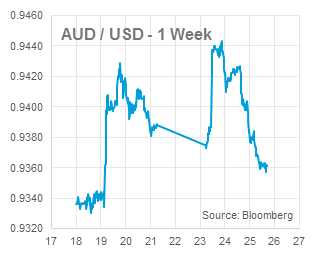

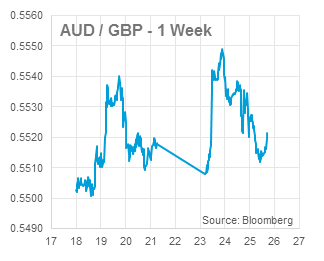

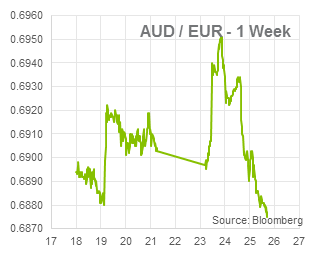

- The HSBC China Flash Manufacturing PMI, a survey of Chinese manufacturing activity, unexpectedly increased to 50.8. The figure indicated industry expansion for the first time since December 2013, causing the AUD to jump against most major currencies. The HSBC economists note that the increase is the result of mini-stimulus programs filtering through the economy with expectations of more to come.

- New Zealand’s economy grew by 1.0% in the quarter to March 2014 driven by construction activity.

USD – The FOMC

Last Thursday, the Federal Open Market Committee pressed on with tapering coupled with its current dovish stance on interest rates. The Fed will now purchase $35 billion worth of mortgage and treasury bonds per month. Though outcomes were fairly widely expected, the USD fell on the release as the statement read slightly more dovishly than expected.

Last Thursday, the Federal Open Market Committee pressed on with tapering coupled with its current dovish stance on interest rates. The Fed will now purchase $35 billion worth of mortgage and treasury bonds per month. Though outcomes were fairly widely expected, the USD fell on the release as the statement read slightly more dovishly than expected.

There was no mention of the latest run of higher than expected inflation. Most pundits reckon the Fed is happy to let inflation run higher than the 2% target so long as it supports the economic recovery. Additionally, the committee were unanimous in their votes for the decision meaning the status quo will likely be maintained in the near term; all things being equal.

It was not all smooth sailing, however. In the press conference, Chairwoman Janet Yellen voiced some concerns about risks to financial stability including unusually low levels of volatility and the products of this. Referring to volatility she stated, “This environment of low volatility is very much on my radar screen and would be a concern to me if it prompted an increase in leverage or other kinds of risk-taking behavior that could unwind in a sharp way.” Increased risk taking has been fostered by ultra-low monetary policy and low expected and actual volatility show that market participants may be overconfident or complacent.

Regarding leverage and increased debt issuance risk, “Trends in leverage lending in the underwriting standards there, diminished risk spreads in lower-grade corporate bonds, high-yield bonds have certainly caught our attention.” The mispricing of debt securities was the main cause of the global financial crisis in 2008 and volatility levels are currently at or below levels seen just prior to this crisis.

GBP by Jeremy Cook, London

Not since the imposition of the Bank of England’s forward guidance plan has the glare on it and doubts around it been so strong. The essence of the forward guidance plan is to tie down investor and borrower expectations as to the path of interest rate rises via increased communication from the central bank.

Not since the imposition of the Bank of England’s forward guidance plan has the glare on it and doubts around it been so strong. The essence of the forward guidance plan is to tie down investor and borrower expectations as to the path of interest rate rises via increased communication from the central bank.

This started as a definitive lock with the UK unemployment rate and an expectation that rates would not rise until that rate hit 7%, something the Bank of England did not forecast until 2016. Once unemployment broke below the 7% level in February, this guidance was quickly repositioned.

As we wrote at the time, with the Bank of England unable to meaningfully target unemployment for interest rate increases, it seems that forward guidance is now closer to forward suggestion; the plan is to keep rates low after the threshold has been hit – much like the Federal Reserve’s forward guidance had changed in the past few months as it has become clear that job increases have come on quicker than had been expected.

The argument for not putting a de facto target in sand became obvious; just as much as they met this threshold in double-quick time that is not to say that another threshold would be met within the MPC’s timeframe. Unfortunately the inherent lack of a target with the Bank’s revised plans led to a different question; how are everyone from City economists to households and businesses expected to interpret this? Increased communications from the Bank of England were the key. Carney relied on the soft sell.

Unfortunately, the clarity around these communications has been sadly lacking. Last month’s Quarterly Inflation Report from the Bank of England dripped with dovishness; emphasis was placed on the low level of inflation, lower still levels of real wage growth and doubts over the amount of slack in the UK economy.

In the past 10 days, the change in tone of Bank of England communications has changed dramatically. Firstly, Carney’s Mansion House speech of 10 days ago carried as its central message that borrowers and investors, businesses and individuals should be prepared for rate rises, but then last Wednesday’s Bank of England minutes suggested a “surprise at the low probability of a 2014 rate increase”.

Carney gets a chance to explain this shift and clarify his position this Tuesday morning in a testimony to the House of Commons’ Treasury Select Committee. One Committee member has in the past amounted forward guidance to “a lot of arm waving until the governor tells us when he thinks rates are going to go up or down.” The welcome to the changes in tone are unlikely to be warmly accepted.

It stands to reason that Carney will not want to flip-flop twice in less than a fortnight in his testimony tomorrow and further bullish chatter on the economy will be needed on the prospects for the UK economy. Figures released this morning by the US Commodity Futures Trading Commission pointed to the highest level of bets of further sterling strength in 7 years were made last week – traders will be hoping that Carney continues to bang the drum in the face of the politician’s ire.

EUR & NZD

New Zealand released its Gross Domestic Product numbers last Thursday morning. The report showed the economy growing by 1.0% in the March quarter after 1.2% was expected. The report showed growth driven primarily by increases in construction; the sector expanded at the fastest pace since March 2000. This caused the NZD to jump despite the missed expectation as continued booming housing will require continued rate rises by the Reserve Bank of New Zealand. The bank has raised interest rates at every meeting in 2014 and is expected to continue doing so. With a benchmark interest rate of 3.25%, the highest of developed economies, the NZD has appreciated as a favoured choice for currency carry trades.

Chris Chandler